Before any merger, acquisition, or investment, companies must confirm that their decisions are based on verified facts and information. A due diligence report provides this foundation by summarising findings from a detailed review of the target business. It helps identify potential risks, assess value, and ensure transparency before formal agreements are signed.

What Is a Due Diligence Report?

A due diligence report is a structured document that summarizes verified information collected during an investigation of a company, project, or investment target. It helps stakeholders assess value and identify potential risks.

Such a report typically outlines the scope of the review, sources of information, and analytical methods used during the evaluation. It then presents a summary of findings, conclusions, and recommendations for next steps in the transaction process.

Why Do We Need a Due Diligence Report?

A due diligence report serves as a foundation for informed business decisions. It ensures that investors, buyers, and partners understand the actual condition of a company before completing a deal. This process also protects against hidden liabilities and regulatory breaches that may appear after closing.

The main reasons for preparing such a document include:

Verifying financial accuracy and performance trends.

Detecting legal obligations, claims, or unresolved disputes.

Revealing operational inefficiencies or hidden expenses.

Assessing market position, growth potential, and competition.

Reviewing management competence and internal policies.

Evaluating the reliability of IT systems and data protection.

Identifying supplier concentration and dependency risks.

Supporting transaction terms and value negotiations.

Assisting with post-deal integration and management.

Building investor and board confidence through transparency.

By completing this review, businesses reduce uncertainty and establish a factual base for negotiations, contract drafting, and long-term planning. It also strengthens investor trust and improves the quality of decision-making at every stage of a transaction.

Types of Due Diligence Reports

Due diligence examines various areas depending on the deal, industry, and company size. Each type focuses on a specific aspect of business operations, providing a comprehensive view of performance, stability, and compliance.

Financial Due Diligence

Assesses resource management and financial stability, including: audited/unaudited statements, cash flow, tax compliance, debt, forecasts, and accounting policies. It confirms whether numbers are reliable and obligations can be met.

Legal Due Diligence

Reviews legal standing, contracts, licenses, IP, litigation, and regulatory compliance to prevent hidden claims and post-deal conflicts.

Operational Due Diligence

Evaluates efficiency and sustainability of daily operations: production, cost control, maintenance, technology use, and reporting structures. It ensures the business model can deliver stable performance.

Commercial / Market Due Diligence

Analyzes market position, growth potential, competition, pricing, sales channels, and customer retention to define realistic targets and reduce valuation risks.

HR / Management Due Diligence

Examines leadership, workforce stability, turnover, compensation, compliance, and succession planning, revealing if people and culture support strategic goals.

IT / Cybersecurity Due Diligence

Assesses software, hardware, network security, data privacy, IT governance, and incident response to prevent disruptions and protect sensitive data.

Vendor / Supplier Due Diligence

Focuses on third-party relationships, supplier contracts, delivery, quality, concentration risk, and ethical compliance to safeguard operations and reduce interruptions.

How to Write a Due Diligence Report Sample

Writing a due diligence report of a company requires a clear process, structured analysis, and consistent documentation. The report should present verified data in a manner that enables decision-makers to assess risks and draw informed conclusions. Each section must be fact-based, objective, and supported by credible sources.

The preparation of a due diligence report usually involves several stages:

Collect and verify all available financial, legal, and operational data.

Conduct interviews with management and relevant stakeholders.

Analyze the findings and identify critical risks or inconsistencies.

Evaluate how these factors may affect valuation or deal terms.

Summarize insights into clear and structured sections.

Prepare appendices with documents, charts, and references.

Each part of the report must lead logically to the next one. The financial review supports the legal and operational sections, while the risk summary connects all findings into a complete picture.

When writing, clarity and structure are essential. Each section should start with a short overview, followed by detailed findings and a concise conclusion. Tables, bullet points, and visuals may be used to make complex information easier to read and interpret.

The final version of the report should undergo internal review and fact-checking before being shared with investors or management. It ensures that the document is accurate, balanced, and suitable for decision-making.

What Should Be in a Due Diligence Report?

A comprehensive due diligence report for a company should encompass all information that enables investors or partners to assess its financial health, legal standing, and operational capabilities. The document must be structured so that readers can easily trace conclusions back to verified data sources.

Typical sections of a due diligence report include:

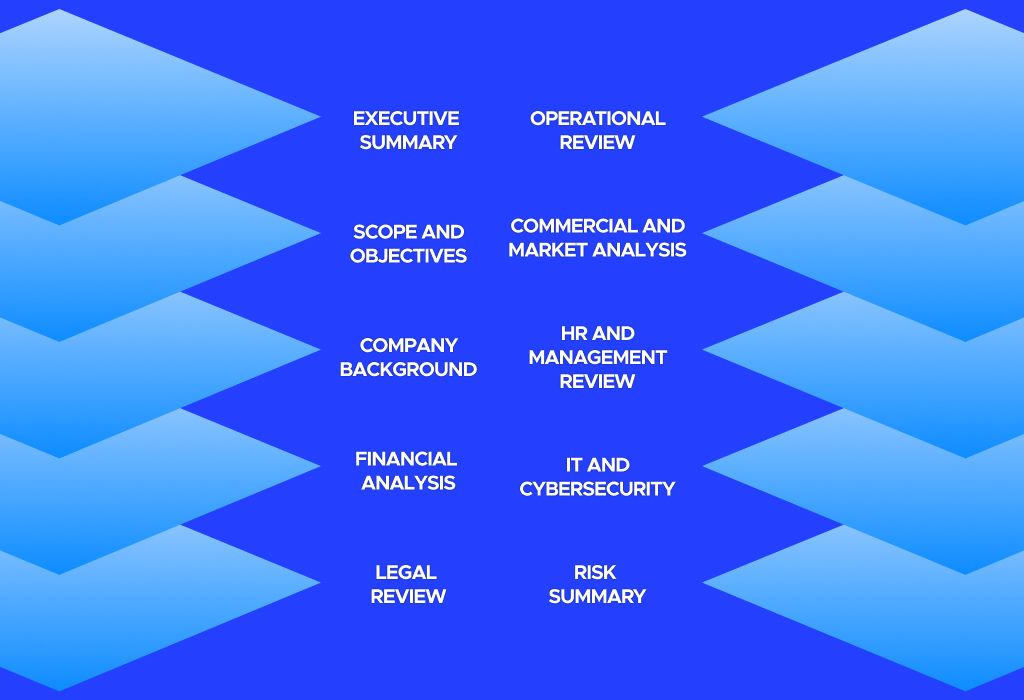

Executive summary: a short overview of purpose, scope, and significant findings.

Scope and objectives: define what areas were reviewed and which data sources were used.

Company background: brief information about ownership, history, and market presence.

Financial analysis: results of balance sheet, cash flow, and profitability review.

Legal review: corporate structure, contracts, intellectual property, and compliance.

Operational review: production, logistics, supply chain, and resource efficiency.

Commercial and market analysis: position, customers, competitors, and forecasts.

HR and management review: leadership quality, staff structure, and labour policies.

IT and cybersecurity: data protection, systems reliability, and infrastructure risks.

Risk summary and recommendations: identified threats and proposed mitigation steps.

Appendices: supporting documents, charts, and additional materials.

Each section should clearly state both strengths and weaknesses of the reviewed company. The goal is to present facts that help decision-makers assess overall stability and prospects.

A well-organised structure also helps ensure comparability between different reports. When due diligence is performed for multiple targets, consistency in layout and terminology facilitates easier cross-analysis and informed decision-making.

What Is a Due Diligence Questionnaire?

A due diligence questionnaire (DDQ) is a structured list of questions sent to a target company before or during the review process. It helps gather essential information quickly and ensures that the same areas are covered in each transaction. The questionnaire simplifies data collection and reduces the risk of missing critical details.

Common topics covered in a due diligence questionnaire include:

General company information and ownership details.

Financial statements, budgets, and forecasts.

Corporate structure, subsidiaries, and shareholders.

Key contracts, licenses, and regulatory approvals.

Pending or potential litigation and compliance matters.

Intellectual property and technology assets.

Human resources policies and employment data.

Using a questionnaire ensures a consistent and systematic approach to due diligence. It also helps both parties understand expectations and prepare supporting documents in advance.

A completed DDQ serves as the foundation for a deeper analysis. The answers highlight where further verification or clarification is needed, helping the reviewing team focus on high-risk or complex areas during the next stage of the process.

Conclusion

A due diligence report consolidates financial, legal, operational, commercial, HR, IT, and supplier insights into a structured document. Proper preparation enhances transparency, mitigates risks, and supports strategic planning. Using a consistent format and referencing sample reports ensures reliability and clarity, enabling stakeholders to assess opportunities and challenges effectively before finalizing any transaction.