Mergers and acquisitions are among the most complex decisions for corporate leadership. Each transaction involves financial risk, strategic opportunities, and investor scrutiny. To evaluate the immediate financial consequences of a deal, professionals frequently rely on accretion/dilution analysis. This approach measures how the acquisition will change the acquiring company's earnings per share (EPS). If the post-deal EPS is higher than the standalone figure, the transaction is accretive. If it decreases, the deal is dilutive.

EPS impact often shapes initial investor reaction and board approval. Still, while accretion can indicate shareholder value creation, and dilution may raise concerns, EPS should never be the only metric guiding strategic decisions. Proper understanding requires attention to assumptions, sector context, and long-term value generation.

Understanding the Basics of Accretion and Dilution

The concept of accretion is straightforward: a deal increases EPS, signaling that shareholders are likely to benefit. Dilution means EPS falls, which can suggest reduced short-term returns. However, the implications are rarely so simple.

For instance, Company A may report EPS of $3.00. After acquiring Company B, its pro forma EPS could reach $3.20. At first glance, the deal is accretive. Yet if leverage increases sharply, the company may face downgraded credit ratings. Conversely, a deal that lowers EPS to $2.80 may appear dilutive, but if it secures new technology or global market access, long-term earnings could grow significantly.

Therefore, accretion and dilution serve as critical but partial indicators. They offer a clear view of the impact of short-term earnings, but must be integrated with broader strategic evaluation.

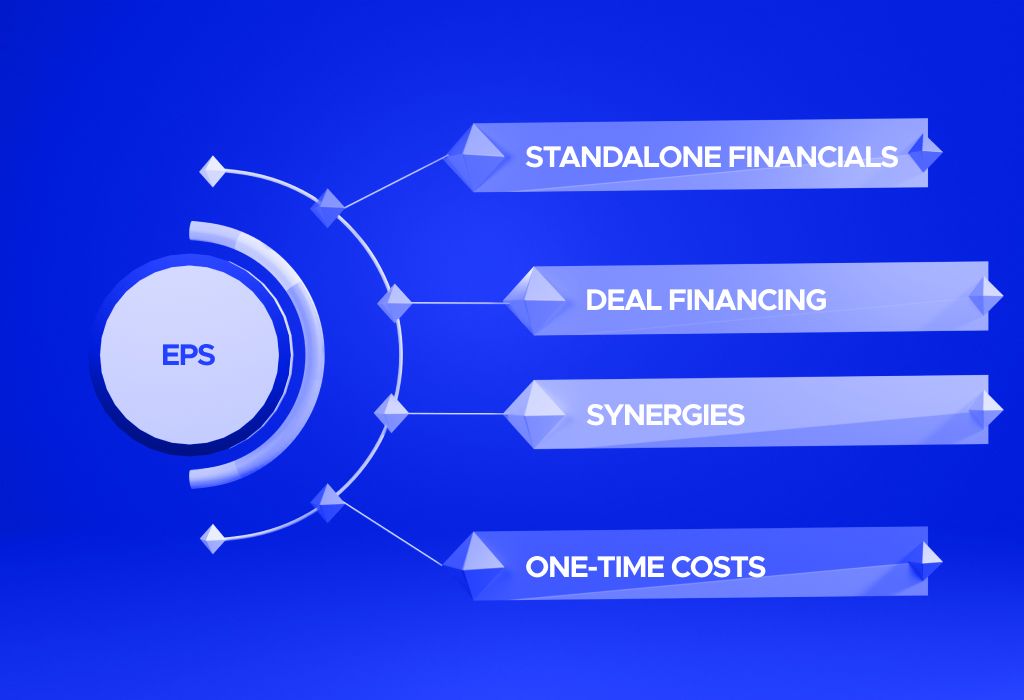

Key Inputs Required for Accretion/Dilution Analysis

Accurate modeling depends on a defined set of inputs. Each component has a measurable influence on EPS forecasts, and misjudging even one can distort the results.

Standalone Financials of Both Companies

A reliable baseline begins with forecasts for both acquirer and target. These include projected revenue growth, margin expectations, working capital needs, and planned capital expenditures. The credibility of the accretion/dilution model rests on the quality of these standalone assumptions.

Deal Structure and Financing Method

The financing approach fundamentally shapes EPS outcomes:

Cash financing reduces liquidity but avoids share dilution.

Debt financing increases leverage and interest expense.

Equity financing expands the share base, potentially lowering EPS despite higher net income.

Blended structures add complexity. Analysts must model scenarios where debt costs rise or stock prices fluctuate before closing. Such sensitivity checks help evaluate whether EPS outcomes are resilient or fragile.

Synergies and Cost Savings

Synergies are often the cornerstone of the acquisition rationale. These include procurement savings, reduction of duplicate staff functions, and cross-selling opportunities. Analysts must determine whether synergies are one-time or recurring and whether they can be realized within the forecast period. Overly optimistic synergy assumptions are a leading reason for later deal underperformance.

One-Time and Ongoing Deal Costs

M&A transactions incur advisory fees, integration expenses, IT system upgrades, and compliance costs. If ignored, these items may make a dilutive transaction appear accretive. Distinguishing between one-time restructuring charges and ongoing expenses ensures clarity in EPS forecasts.

Step-by-Step Calculation Overview

A standard accretion/dilution analysis follows a clear sequence:

Collect standalone net income and EPS for both companies.

Adjust for deal financing—reductions in cash, additions of debt service, or expanded share count.

Add expected synergies to pro forma income.

Deduct integration and recurring costs.

Calculate the combined net income and divide by the new share base.

Compare the acquirer's post-deal EPS with the pre-deal EPS.

For example, if the acquirer's standalone net income is $500 million with 250 million shares outstanding, EPS equals $2.00. After the deal, net income grew to $650 million, but share count expanded to 325 million. EPS becomes $2.00, showing no accretion despite the income increase. Such outcomes illustrate why EPS effects are not always intuitive.

Using Consensus EPS and Analyst Estimates

Analyst estimates serve as a critical reference point. Relying solely on management forecasts may create unrealistic expectations. Consensus EPS figures, derived from multiple research sources, reflect the broader market view. Using these estimates ensures the model aligns with investor assumptions and provides greater transparency when presenting the deal to boards or shareholders.

Interpreting the Results: Beyond the Numbers

The numerical outcome—accretive or dilutive—is only the starting point. The strategic interpretation matters more. Investors evaluate:

Whether leverage increases or reduces future flexibility.

How realistic does the synergy timeline appear?

Whether the acquisition expands market share or strengthens technology.

In industries with strict regulatory oversight, such as banking or pharmaceuticals, investors place additional emphasis on compliance costs and integration challenges. By contrast, in technology or telecom, speed of integration and market expansion may carry greater weight.

Sector-Specific Considerations

The importance of accretion/dilution varies by industry:

Banking and financial services. EPS accretion is closely tied to capital adequacy and regulatory ratios.

Pharmaceuticals. Synergies often come from consolidating R&D pipelines and sales networks.

Energy and utilities. Cost synergies dominate, but regulatory approval may delay benefits.

Technology/ Strategic value, such as acquiring platforms or intellectual property, can justify near-term dilution.

These variations highlight the importance of context. The same EPS impact may be received differently depending on the sector and its growth profile.

Limitations and Pitfalls of the Model

Accretion/dilution analysis provides clarity but has inherent limitations. It focuses narrowly on EPS, which is an accounting measure rather than a direct proxy for value. Common pitfalls include:

Ignoring free cash flow implications.

Overestimating synergy capture.

Underestimating cultural or operational integration risks.

Relying on accounting policies that differ under IFRS and US GAAP.

Analysts must remind stakeholders that EPS changes cannot fully capture risk-adjusted value creation.

Advanced Modeling Approaches

Beyond simple models, advanced techniques provide greater insight. Scenario analysis allows for optimistic, base, and conservative projections. Monte Carlo simulations test probability distributions for uncertain variables like synergy realization or debt costs. Technology-enabled platforms incorporate real-time market data, while AI-driven tools assist in identifying risk factors hidden in financial statements. These methods increase precision and reduce reliance on single-point estimates.

Governance, Communication, and Market Perception

How the results are communicated is as important as the results themselves. Investor relations teams must explain the drivers of accretion or dilution clearly and transparently. Boards and risk committees evaluate whether assumptions are credible, while rating agencies examine leverage and debt service coverage. Effective communication helps prevent negative market reaction, especially when a transaction shows near-term dilution but promises long-term growth.

Tools and Best Practices for Analysts and Deal Teams

Accretion/dilution analysis requires more than running standard calculations. To ensure accuracy and credibility, analysts and deal teams should combine financial discipline, advanced tools, and clear communication. The following practices form a unified framework that supports reliable outcomes:

Run sensitivity and scenario testing by adjusting variables such as interest rates, synergy capture, integration costs, and share price movements to assess how results change under different conditions.

Integrate EPS forecasts with cash flow modeling to confirm that accretive finance outcomes also translate into liquidity improvement and debt service capacity.

Apply consistent methodologies across multiple transactions, enabling boards and executives to compare potential deals on a uniform basis and avoid misleading contrasts.

Document all assumptions transparently, including synergy timelines, financing costs, and tax effects, so regulators, auditors, and rating agencies can evaluate the credibility of the analysis.

Leverage specialized financial modeling tools and technology, such as advanced spreadsheet models, dedicated M&A platforms, and simulation techniques like Monte Carlo analysis, to improve accuracy and reduce human error.

Coordinate with governance and communication teams to ensure that the results of accretion/dilution analysis are explained clearly to boards, shareholders, and rating agencies, avoiding misinterpretation of headline figures.

Establish a feedback loop after deal completion by comparing projected EPS outcomes with actual results, refining assumptions, and building organizational knowledge for future transactions.

By applying this integrated set of practices, deal teams enhance the reliability of their models, strengthen market confidence, and reduce the risk of overstating the benefits of potential acquisitions.

Conclusion – Accretion/Dilution as One Piece of the Puzzle

Accretion dilution analysis remains one of the most practical tools for evaluating mergers and acquisitions. It offers a clear view of how EPS will be affected, helping investors and executives judge immediate financial outcomes. Yet its limitations are equally clear. EPS growth may reflect accounting gains rather than sustainable value, while dilution may hide strategic advantages.

An effective evaluation framework considers EPS alongside free cash flow, debt sustainability, market positioning, and long-term competitive advantages. A transaction that is accretive in the short term can erode shareholder value if integration fails, while a dilutive deal can generate strong returns if it strengthens the company's strategic foundation.

For deal teams, boards, and investors, the lesson is simple: accretion/dilution analysis is indispensable, but never sufficient on its own. Used with discipline and combined with broader valuation methods, it helps ensure that mergers and acquisitions create real, lasting value.