Before assessing a company’s worth, investors must understand that there is more than one way to measure its value. Two of the most common indicators—market capitalization and enterprise value—describe different perspectives on the same business. Knowing how they differ helps analysts, shareholders, and potential buyers interpret financial data correctly and make informed decisions.

What Is Market Capitalization?

Market capitalization, often called market cap, represents the total market value of a company’s outstanding shares. It is calculated by multiplying the current share price by the total number of issued shares.

This figure represents the market's valuation of the company’s equity at a particular moment. It provides a simple way to compare businesses within the same sector and is often used for classification into large-cap, mid-cap, or small-cap categories.

However, market cap shows only the value of equity. It does not consider debt, cash reserves, or other obligations, which means it can present an incomplete view of a company’s actual worth.

What Is Enterprise Value (EV)?

Enterprise value (EV) offers a broader measure of a company’s total value. It represents the combined worth of both equity and debt, adjusted for available cash.

EV is calculated using the formula:

EV = Market Cap + Total Debt − Cash and Cash Equivalents

This calculation shows how much an investor would theoretically need to pay to acquire the entire company, including its liabilities but excluding cash and cash equivalents. In some instances, the formula also includes preferred stock and noncontrolling (minority) interests to present a more precise estimate.

By accounting for debt and liquidity, enterprise value gives a clearer picture of the company’s overall financial position and investment appeal.

Enterprise Value vs. Market Cap—The Key Differences

Is enterprise value the same as market cap? Although both indicators aim to measure how much a business is worth, they operate from different perspectives. Understanding the difference between market cap and enterprise value is fundamental to accurate financial analysis and fair comparisons between companies.

Market capitalization shows how the equity market values a company’s shares. It reflects investors’ collective expectations of future earnings, growth potential, and market conditions. In contrast, enterprise value represents the total amount an investor would need to acquire the entire business, including responsibility for its debts and access to its cash reserves.

In practical terms, market cap is what shareholders own, while enterprise value is what a potential acquirer would effectively pay. This distinction becomes important in mergers, acquisitions, and leveraged buyouts, where the buyer assumes both assets and liabilities.

The difference between EV and market cap also highlights how capital structure influences valuation. A company with heavy borrowing can appear large by market cap, but much more expensive once debt is considered. Conversely, a firm with strong liquidity and low leverage may have a smaller EV than its market capitalization, suggesting a solid financial position and potentially reduced acquisition costs.

Analysts prefer EV when comparing firms that use different financing strategies. For instance, a company funded mainly through equity will show a higher market cap but a similar EV to a peer financed by debt. Using EV removes these distortions, providing a more consistent basis for valuation.

Key analytical implications include:

Leverage impact. Higher debt raises EV relative to market cap, revealing financial risk.

Cash effect. Large cash reserves reduce EV, signaling greater flexibility or underutilized assets.

Comparability. EV allows cross-industry or international comparisons where debt levels vary.

Acquisition insight. EV estimates the total takeover cost, essential for M&A evaluation.

Operational focus. Ratios based on EV link value to business performance, not short-term stock volatility.

Therefore, while market cap reflects current market sentiment, enterprise value delivers a more complete economic picture. Together, they enable analysts to understand both the perception and the underlying reality of a company’s worth.

Why Enterprise Value Can Be More Accurate

Enterprise value is often considered a more comprehensive metric because it includes financial obligations and liquidity positions that market cap ignores.

It captures the company’s economic footprint by combining its market equity with outstanding debt. If two companies have identical market caps but different debt levels, their EVs will vary substantially.

Analysts also prefer EV for valuation ratios such as EV/EBITDA or EV/Sales. These indicators allow cross-comparison between companies regardless of financing methods or accounting differences.

By including both sides of the balance sheet, EV provides a balanced and reliable estimate of corporate value, especially in transactions or investment analysis.

When Market Cap Is Still Useful

Despite its simplicity, market capitalization remains a valuable tool in several contexts. It is widely used in public markets and is often the first figure investors encounter when evaluating a stock.

Typical use cases include:

Comparing companies with similar debt profiles within the same industry.

Assessing stock-based metrics such as earnings per share or dividend yield.

Defining company size categories for portfolio diversification.

Performing quick evaluations when detailed financial data is unavailable.

Tracking market trends and investor sentiment over time.

In summary, market cap remains a practical indicator of equity value, even though it does not capture the full economic scope that EV provides.

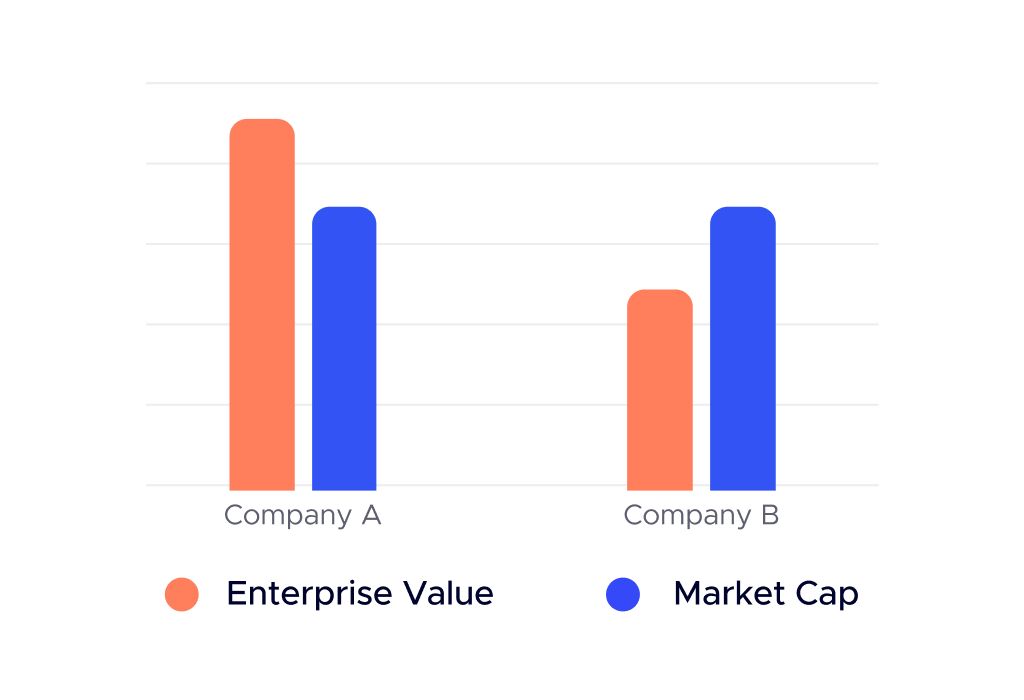

Real-World Example: Comparing Two Companies

Consider two companies with identical share prices and outstanding shares. Their market caps appear the same, suggesting similar valuations.

However, Company A has high debt and limited cash, while Company B holds minimal debt and strong reserves. In this case:

Both firms share the same market cap.

Company A’s EV is significantly higher due to outstanding liabilities.

Company B’s EV may be lower because of its cash balance.

This example shows why EV offers a more accurate representation of business value when debt and liquidity vary between firms.

How to Use EV and Market Cap Together

The most effective approach is to use both indicators together rather than relying on one. Each offers a unique insight into the valuation of a company.

A practical workflow includes:

Begin with the market cap to determine the company’s equity value.

Add total debt and subtract cash to calculate enterprise value.

Use EV-based ratios (EV/EBITDA, EV/Sales) for performance comparison.

Compare EV and market cap to understand capital structure and leverage.

Apply both figures when assessing acquisition targets or investment risk.

This combined approach allows investors to balance simplicity with financial precision.

Common Mistakes When Comparing EV and Market Cap

Analysts sometimes make errors when evaluating EV vs. market cap, leading to misleading conclusions. Frequent mistakes include:

Comparing one company’s EV to another’s market cap.

Excluding off-balance-sheet liabilities such as leases or guarantees.

Using outdated debt figures or ignoring short-term borrowings.

Deducting non-cash assets that are not immediately liquid.

Applying the wrong multiple (e.g., using EV/net income instead of EV/EBITDA).

Treating financial institutions the same way as non-financial firms.

Avoiding these errors ensures that valuations remain consistent and reflect the company’s real economic situation.

Conclusion

Market cap and enterprise value are both essential in financial analysis, but they serve different purposes. Market cap measures the equity portion seen by investors, while EV captures the full scope of a company’s value, including debt and cash.

Using both together provides a balanced perspective—market cap for simplicity and EV for depth. This combination enables analysts and investors to make better comparisons, build stronger valuations, and base strategic decisions on complete financial information.