Main takeaways

Financial due diligence checks whether revenue is real, recurring, collectible, and stable.

EBITDA analysis separates sustainable earnings from one-time items and unsupported add-backs.

Working capital review shows how much operating cash the business needs after closing.

A cash flow analysis reveals whether accounting profit translates into real liquidity.

A debt and liability review identifies obligations that can affect price and SPA terms.

A forecast review tests whether management's projections support valuation.

Financial due diligence helps buyers, investors, and lenders verify a business's true financial condition before a deal. It checks revenue quality, EBITDA, cash flow, working capital, debt, liabilities, accounting risks, and forecasts. In M&A, fundraising, private equity, investments, and acquisition finance, these findings affect valuation, deal structure, and post-closing risks.

What is financial due diligence?

Financial due diligence means a transaction-focused review of a company’s financial position, performance, and risks. It is usually performed before an acquisition, merger, investment round, debt financing, or private equity deal. The main question is simple: Does the business truly generate the results shown by management, and can those results continue after closing?

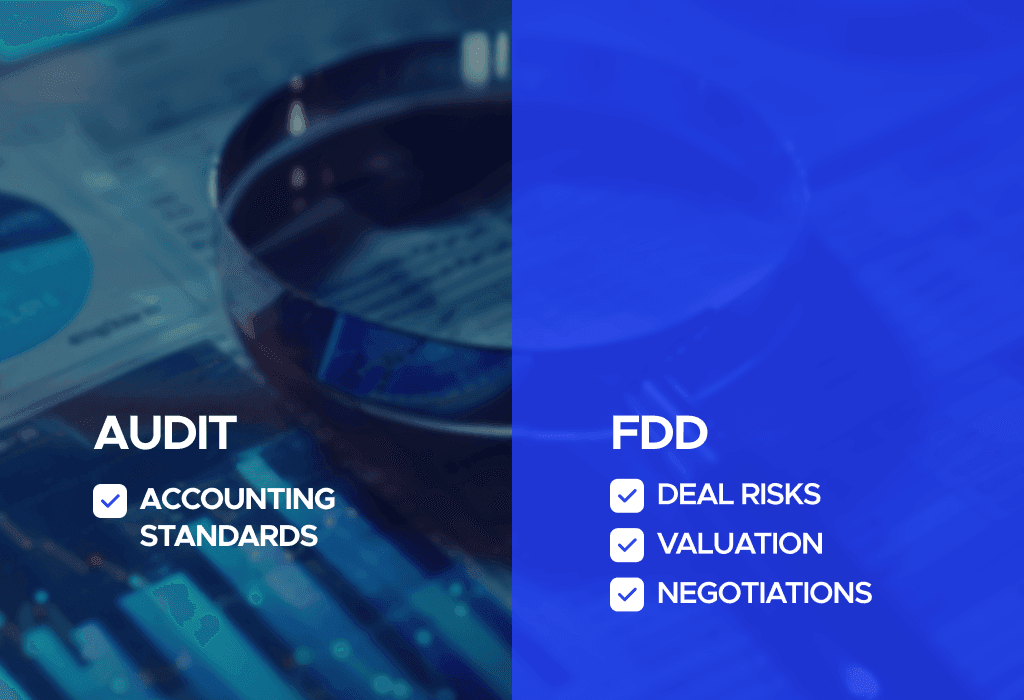

So, what is due diligence in finance? Financial due diligence is different from an audit. An audit checks whether historical financial statements are fairly presented in accordance with accounting standards. It is backward-looking and follows formal rules. Financial due diligence is deal-specific and commercial. It asks whether the numbers support the transaction, what risks may affect valuation, and how findings should be reflected in the purchase agreement.

Main areas covered in financial due diligence

Revenue quality

Revenue quality analysis checks whether reported revenue is real, recurring, collectible, and sustainable. The review covers revenue recognition policies, customer contracts, billing patterns, deferred revenue, returns, discounts, sales by product or geography, and receivables.

The main risks are overstated revenue, one-off sales presented as recurring income, premature revenue recognition, weak collection, and dependence on a small group of customers. If growth depends on discounts, one large customer, or accounting timing, the buyer may view it as lower-quality revenue. This can reduce projected revenue, EBITDA, and valuation, or lead to an earn-out.

EBITDA analysis

EBITDA analysis matters because many businesses are valued using an EBITDA multiple. Analysts start with reported EBITDA and build a normalized EBITDA view. They examine one-time expenses, owner compensation, restructuring costs, litigation costs, unusual income, accounting policy changes, and management add-backs.

The main risk is inflated EBITDA. Sellers may classify regular operating costs as non-recurring or present add-backs that are not supported by documents. If normalized EBITDA is lower than management’s target, valuation may decline, and the buyer may adjust the price, multiple, earn-out formula, or seller warranties.

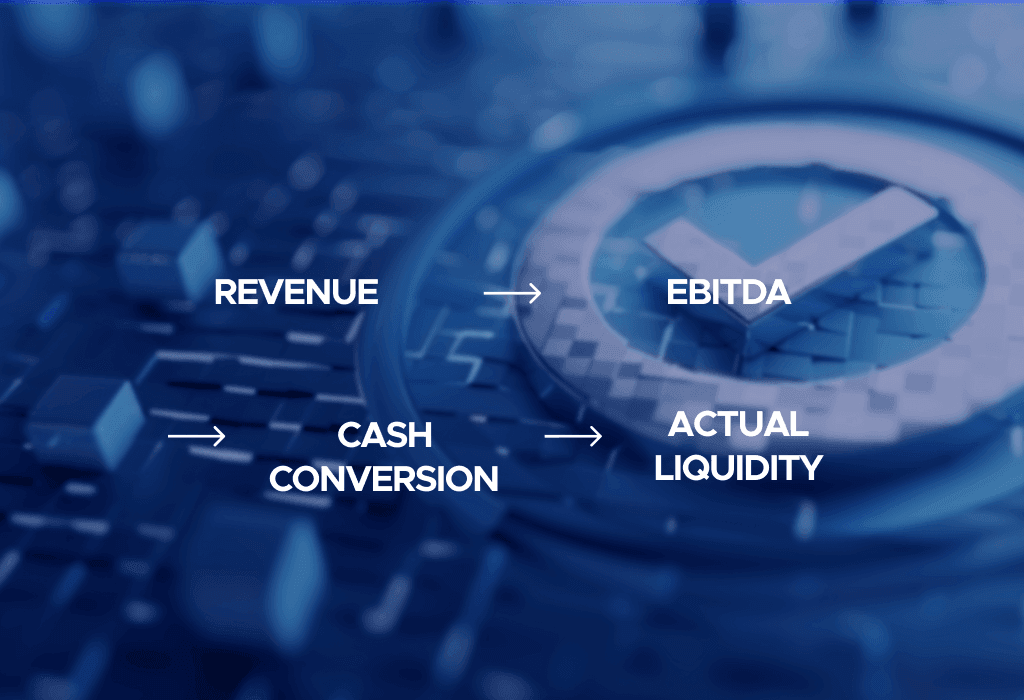

Cash flow review

A cash flow analysis checks whether profits convert into actual cash. A company can report strong EBITDA but still face liquidity pressure due to delayed collections, high inventory levels, heavy capital expenditures, or debt service.

The review covers operating cash flow, free cash flow, cash conversion, capital expenditure, minimum cash needs, debt repayment schedules, and the link between revenue and collections. If receivables grow faster than revenue or the company constantly needs working capital injections, reported earnings may overstate the value available to the buyer.

Working capital analysis

Working capital analysis reviews the capital required to run the business in normal conditions. It covers accounts receivable, accounts payable, inventory, deferred revenue, accrued expenses, and seasonality.

In many M&A deals, the seller must deliver a normal level of net working capital at closing. Financial due diligence helps define that target. Analysts review monthly working capital, calculate DSO, DPO, and inventory days, and identify unusual movements. If actual working capital at closing is below the agreed target, the purchase price may be reduced.

Debt and liabilities

Debt and liabilities review identifies obligations that may reduce equity value. The analysis covers bank debt, shareholder loans, leases, unpaid taxes, guarantees, litigation exposure, supplier arrears, contingent liabilities, and off-balance-sheet commitments.

The main risk is hidden or understated liabilities. A target may have obligations that are not clear from the balance sheet, such as legal claims, tax disputes, deferred payments, or lease commitments. These findings affect valuation through net debt adjustments and can change SPA terms through indemnities, escrow, holdbacks, warranties, or a lower price.

Forecast and financial model review

A forecast review tests whether management's projections are realistic. Analysts examine revenue growth assumptions, margin expansion, pricing plans, customer retention, capital expenditure, hiring plans, and cost structure.

The main risk is an overly optimistic model. A forecast may assume rapid growth without support from historical results, signed contracts, pipeline conversion, or operational capacity. If the model is too aggressive, the buyer may revise valuation, reduce leverage, use a lower multiple, or tie part of the consideration to future results.

Why financial due diligence matters in M&A

Financial due diligence matters because signing is not the end of the risk. Many problems become apparent after closing, when the buyer takes over the company and discovers that the reported performance was less stable than expected.

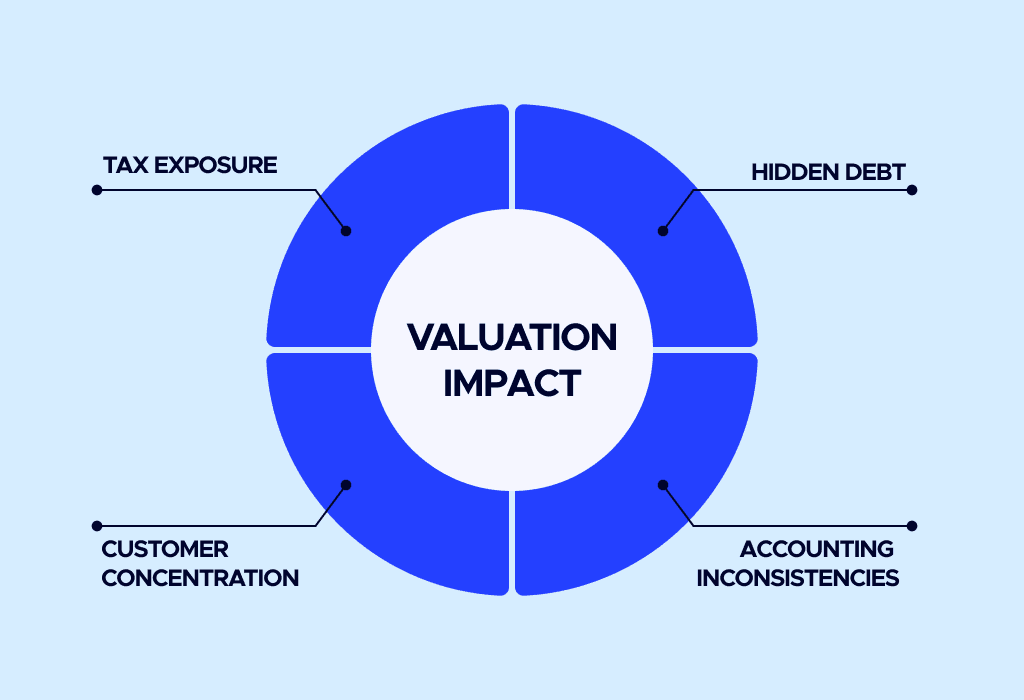

Hidden liabilities are a major concern. A target may have tax exposure, vendor disputes, legal claims, or debt-like items that reduce the business's real value. Without FDD, these issues may be discovered too late.

Overstated revenue is another common problem. A company may accelerate revenue recognition, rely on temporary sales tactics, or present gross revenue when net revenue would be more accurate. Unsustainable margins can also distort valuation if EBITDA improves due to delayed hiring, reduced maintenance, temporary supplier terms, or underinvestment in operations.

Customer concentration creates another risk. If a single customer accounts for a large share of sales, losing that customer can damage future earnings. Accounting inconsistencies add another layer of risk because weak controls or poor reconciliations make it harder to trust the numbers.

FDD findings influence pricing, SPA negotiations, earn-outs, and indemnities. A buyer may reduce the price, request a working capital adjustment, change the definition of EBITDA, demand seller protection for tax or litigation risks, or structure part of the price as an earn-out.

In 2011, Hewlett-Packard acquired the British software company Autonomy for more than $10 billion. One year later, HP announced an $8.8 billion writedown, saying it had discovered serious accounting improprieties, disclosure failures, and misrepresentations related to Autonomy’s financials. Former Autonomy managers denied the allegations, but the deal became one of the most discussed M&A cautionary cases in technology.

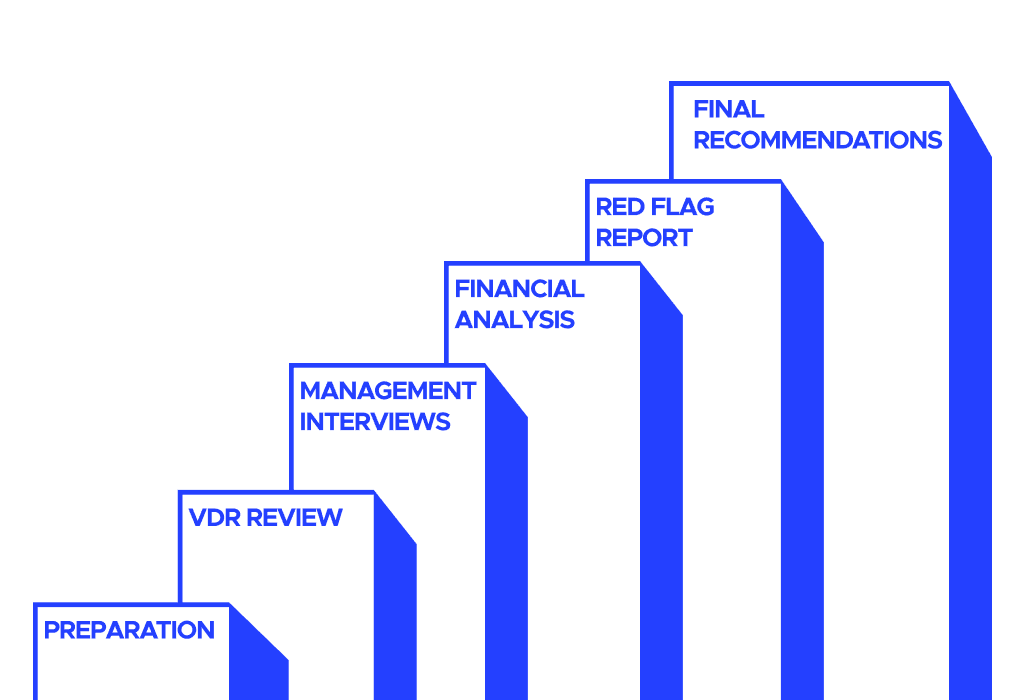

Financial due diligence process step by step

1. Preparation

The process starts with scope definition. The buyer and transaction advisory team decide what must be reviewed, which risks matter most, the applicable timeline, and which documents are required.

2. Data room review

The seller uploads documents into a virtual data room. A structured VDR gives controlled access to financial statements, management accounts, customer contracts, tax returns, debt agreements, budgets, forecasts, and accounting policies. It protects confidential information, tracks access, and centralizes requests.

3. Management interviews

The team interviews management to understand business drivers, accounting policies, revenue recognition, customer retention, cost structure, working capital cycles, and forecast assumptions. These discussions often reveal issues that are not clear in reports.

4. Financial analysis

Advisers normalize EBITDA, test revenue quality, compare profit with cash flow, calculate working capital needs, identify debt-like items, review liabilities, and assess the forecast.

5. Red flag reporting

Advisers may issue red flag reports before the final report. This helps the buyer react quickly if a serious issue appears: unsupported EBITDA adjustments, missing financial data, hidden debt, weak cash conversion, or unusual revenue recognition.

6. Final recommendations

The final report summarizes findings and explains how they affect valuation and deal structure. It may recommend price adjustments, SPA protections, working capital mechanisms, earn-out conditions, indemnities, escrow, or post-closing control improvements.

Common financial due diligence red flags

Aggressive revenue recognition is a serious warning sign. If revenue is recorded before delivery, before customer acceptance, or without reasonable certainty of collection, reported growth may be unreliable.

Inconsistent reporting is another red flag. If management accounts, tax filings, and financial statements do not reconcile, the buyer needs to understand why. Missing schedules or unexplained accounting changes can point to deeper accounting risks.

Weak internal controls increase the risk of errors or fraud. Warning signs include poor segregation of duties, manual reconciliations, lack of approval procedures, and limited finance oversight.

Customer dependency can change the investment case. If a single large customer drives a major share of revenue, the buyer should review contract terms, renewal history, pricing, termination rights, and the stability of the relationship.

Cash flow mismatch is another concern. If EBITDA grows but operating cash flow remains weak, the business may be consuming cash through receivables, inventory, or capital expenditure.

Conclusion

Financial due diligence tests whether the financial story behind a business is reliable, sustainable, and priced correctly. It connects financial statements with deal negotiation, valuation adjustments, acquisition finance, accounting risks, and post-deal planning.

For M&A, private equity, fundraising, and lending, financial due diligence shapes valuation, SPA wording, earn-outs, indemnities, and the buyer’s ability to manage risk after closing.

FAQ

What is included in financial due diligence?

Financial due diligence usually includes revenue quality, EBITDA normalization, cash flow analysis, working capital analysis, debt and liabilities review, tax exposure review, and forecast testing.

How long does financial due diligence take?

The timeline depends on deal size, industry, data quality, and transaction complexity. A focused review may take several weeks; larger cross-border or private equity deals can take longer.

What is the difference between audit and due diligence?

An audit checks whether historical financial statements are fairly presented in accordance with accounting standards. Financial due diligence evaluates whether the business is worth buying at the proposed price and what risks may affect the transaction.

Who performs financial due diligence?

Financial due diligence is usually performed by transaction advisory firms, accounting firms, financial consultants, and tax advisers.

Can financial due diligence affect valuation?

Yes. FDD findings can lead to valuation adjustments, lower EBITDA, revised working capital targets, net debt adjustments, earn-outs, indemnities, or changes to the purchase agreement.