Key takeaways

Choosing M&A financing balances cost of capital, control, and flexibility.

Senior debt, acquisition debt, and bonds can support larger deals, but add debt service, covenants, and refinancing risk.

Equity financing preserves cash flow and avoids mandatory repayment, but causes dilution and may reduce buyer control.

Mezzanine financing, preferred equity, seller notes, and earn-outs can bridge funding gaps and valuation disagreements.

Seller financing and rollover equity improve certainty when default, priority, governance, and exit terms are clear.

Financing due diligence relies on forecasts, working capital, cap tables, commitment letters, and VDR audit trails.

Financing an acquisition is not merely a task of raising capital. It determines risk allocation, control, covenants, ownership, and flexibility. Most transactions use a mix of cash, debt, equity, and deferred payments, with the chosen structure reflected in due diligence, commitment documents, and the purchase agreement.

What Is M&A Financing?

M&A financing refers to the methods buyers use to fund the acquisition of a target company. It may be needed by a strategic acquirer, private equity sponsor, management team, or acquisition vehicle when the price exceeds available cash or liquidity should be preserved.

The source of funds affects structure, leverage, and closing certainty. It is linked to enterprise value, equity value, working capital adjustments, acquisition debt, SPA conditions, and the timetable. Buyers evidence funds through cash proof, term sheets, commitment letters, loan agreements, subscriptions, and board approvals. In corporate finance M&A, a fully funded buyer may be more credible than a higher bidder, depending on broad lender conditions.

Main M&A Financing Methods

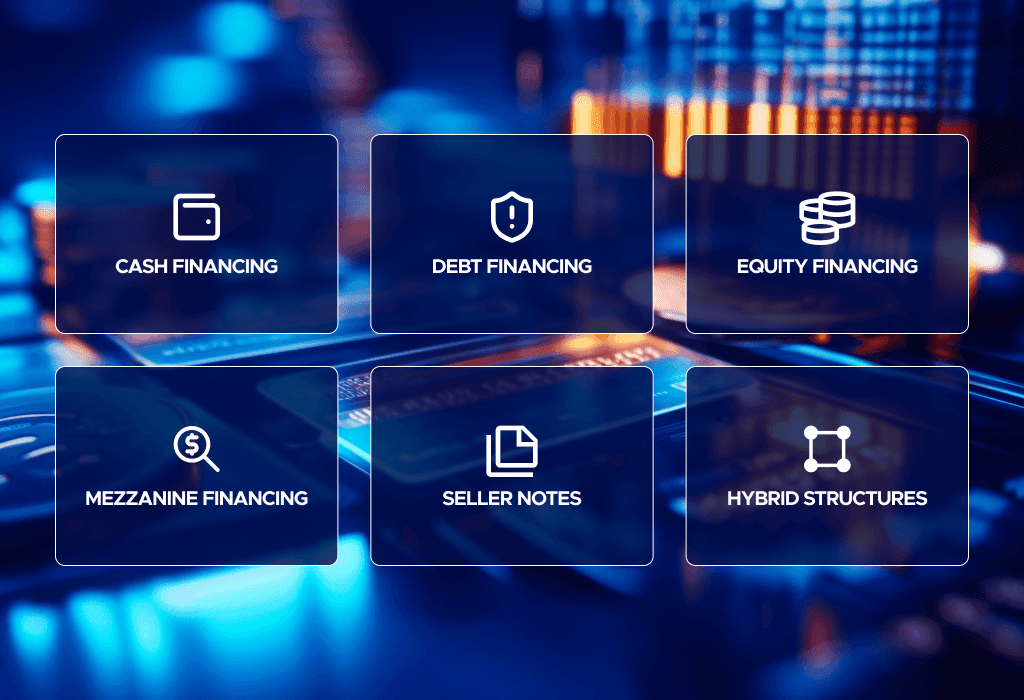

The main methods of financing mergers and acquisitions are cash, debt, equity, and hybrid structures. Most deals combine several methods because each affects control, dilution, leverage, and execution.

Cash Financing. Cash is simple and can increase seller confidence because it avoids lender approval, dilution, and complex conditions. The buyer’s risk is reduced liquidity for integration, working capital, and capex.

Debt Financing. Debt may include senior debt, acquisition debt, term loans, RCFs, bridge loans, or bonds. It preserves ownership but introduces debt service, lender review, covenants, and security packages.

Equity Financing. Equity may involve buyer shares, sponsor equity, minority investors, or stock-for-stock consideration. It reduces mandatory repayment pressure, but dilutes owners and exposes sellers to liquidity, valuation, and market risk.

Mezzanine Financing. Mezzanine capital sits between senior debt and equity. It can fill a funding gap, but usually has higher pricing, subordination, and possible warrants, PIK interest, or conversion rights.

Seller Financing and Seller Notes. Seller financing lets the seller accept part of the price over time, often through a seller note or vendor financing. It needs clear maturity, interest, default, security, subordination, and set-off terms.

Earn-Outs and Deferred Consideration. Earn-outs link part of the price to future revenue, EBITDA, customer, or product milestones. They require precise metrics, accounting policies, reporting rights, and dispute procedures.

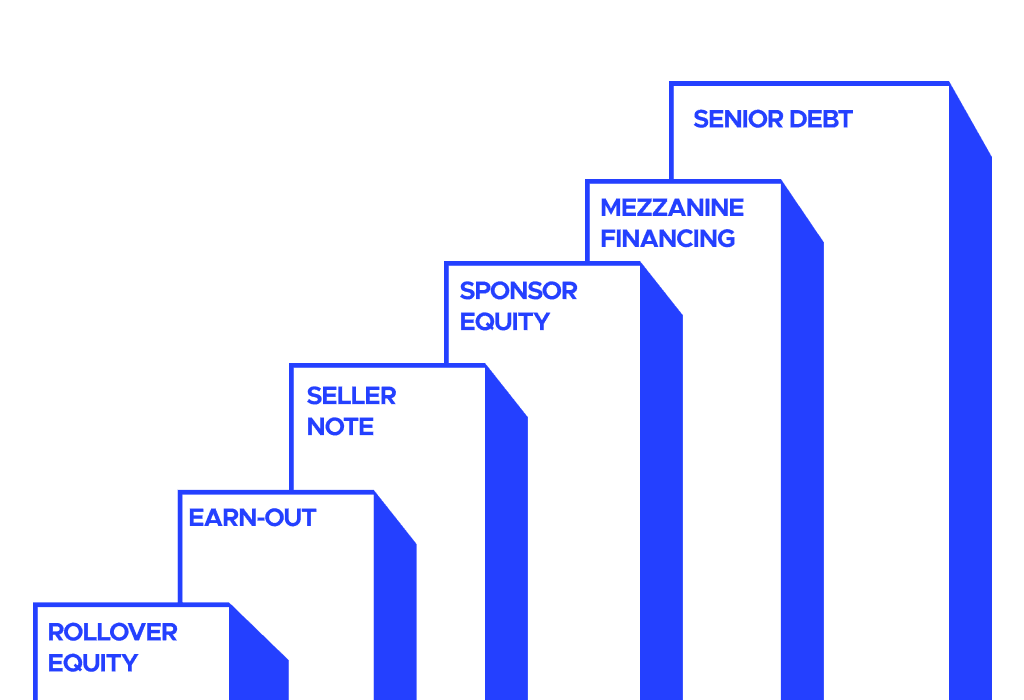

Hybrid Financing Structures. Hybrid structures combine sponsor equity, senior debt, preferred equity, rollover equity, seller notes, and earn-outs. They improve flexibility but increase complexity around priority, control rights, and accounting treatment.

Ultimately, the goal is not to select the cheapest source of funding, but the one that offers the highest degree of closing certainty without crippling the target’s future flexibility. An over-reliance on debt can lead to covenant breaches, while excessive equity issuance may frustrate existing shareholders.

Debt Financing in M&A

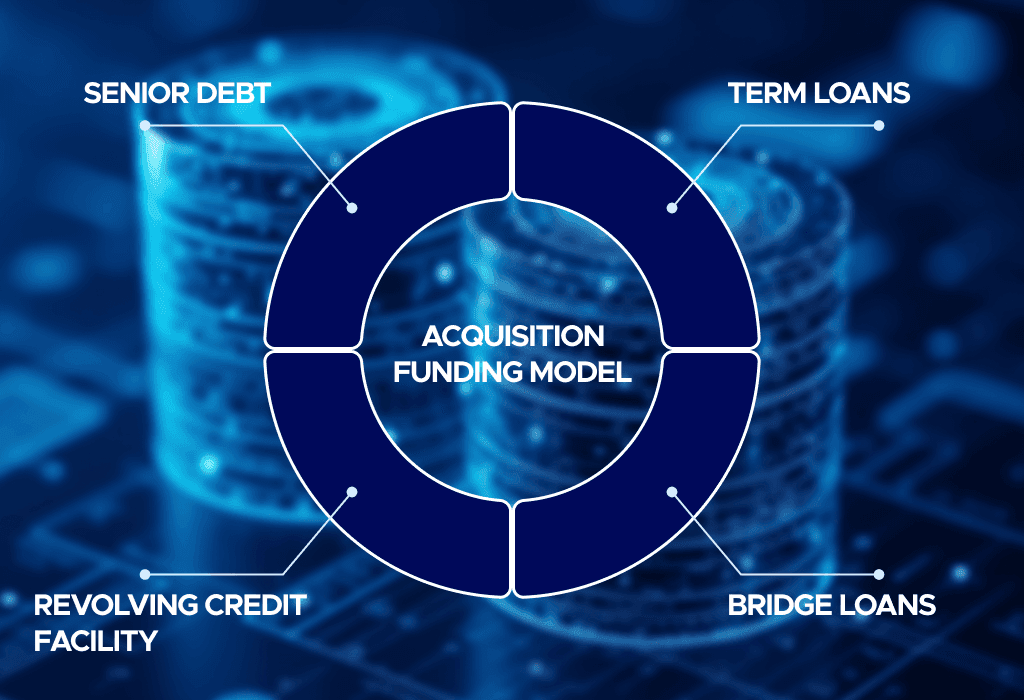

Debt financing is central to many acquisitions and leveraged buyouts. Senior debt sits at the top of the capital stack and may be secured by target assets, shares, receivables, inventory, equipment, intellectual property, or bank accounts. Lenders review EBITDA, cash flow, working capital, debt-like items, forecasts, and integration costs to assess repayment capacity.

Term loans provide acquisition funding, while a revolving credit facility supports liquidity and working capital. Bond financing may suit larger transactions, and bridge loans can cover funding gaps. Debt reduces dilution, but excessive leverage increases closing risk through interest expense, amortisation, covenants, collateral requirements, and refinancing pressure.

A recent high-profile example is Elon Musk’s $44 billion acquisition of Twitter, now X. Reuters reported that the deal was supported by about $13 billion of debt, including a $6.5 billion secured term loan, a $500 million revolving credit facility, $3 billion of unsecured loans, and $3 billion of secured loans. After closing, banks struggled to sell the debt to investors because of uncertainty around the company’s revenues and default risk.

Equity Financing in M&A

Equity financing funds the acquisition through buyer shares, sponsor equity, minority investor capital, rollover equity, or stock-for-stock consideration. It is common where the target is high-growth, cash flows are volatile, debt markets are difficult, or the buyer wants to preserve liquidity.

For sellers, equity may offer future upside, but it creates valuation, liquidity, and market risk. Public company shares may require approval or lock-up restrictions. In private equity deals, sponsor equity may improve lender confidence, while rollover equity can align founders or management with post-closing performance. The trade-off is dilution, less control, and exit dependence.

A well-known example is Disney’s acquisition of 21st Century Fox. Reuters reported that Disney increased its offer to $71.3 billion and used a cash-and-stock structure, with Fox shareholders expected to own about 19% of the combined company after closing.

Hybrid Structures: Mezzanine, Seller Notes and Earn-Outs

Hybrid structures are used when one funding source is insufficient or when parties want to share risk. They include mezzanine financing, preferred equity, seller notes, vendor financing, earn-outs, rollover equity, and minority co-investment.

Mezzanine financing is subordinated debt or preferred equity with features such as warrants, conversion rights, or PIK interest. It can reduce common equity needs, but ranks behind senior lenders and may create refinancing pressure. Seller notes and vendor financing make the seller a creditor of the buyer; they can increase closing certainty, but expose the seller to credit risk.

Earn-outs defer value until the target achieves agreed milestones. They can bridge valuation gaps, but create disputes if metrics are vague or the buyer controls performance drivers. Preferred equity can reduce repayment pressure, but may complicate governance, priority, and accounting treatment.

How Buyers Choose the Right Financing Mix

There is no universal best mix. Buyers assess deal size, balance sheet strength, target cash flow stability, cyclicality, interest environment, risk appetite, seller expectations, regulatory approvals, lender support, integration costs, and expected synergies. Corporate finance and M&A teams should model several structures rather than assume debt is always cheaper or equity is always safer.

Stable businesses with predictable revenue and manageable working capital may support more leverage. Volatile targets may require more equity, seller financing or earn-outs. A fully funded bid may be stronger than a higher bid with uncertain lender commitment.

Financing Due Diligence and Required Documents

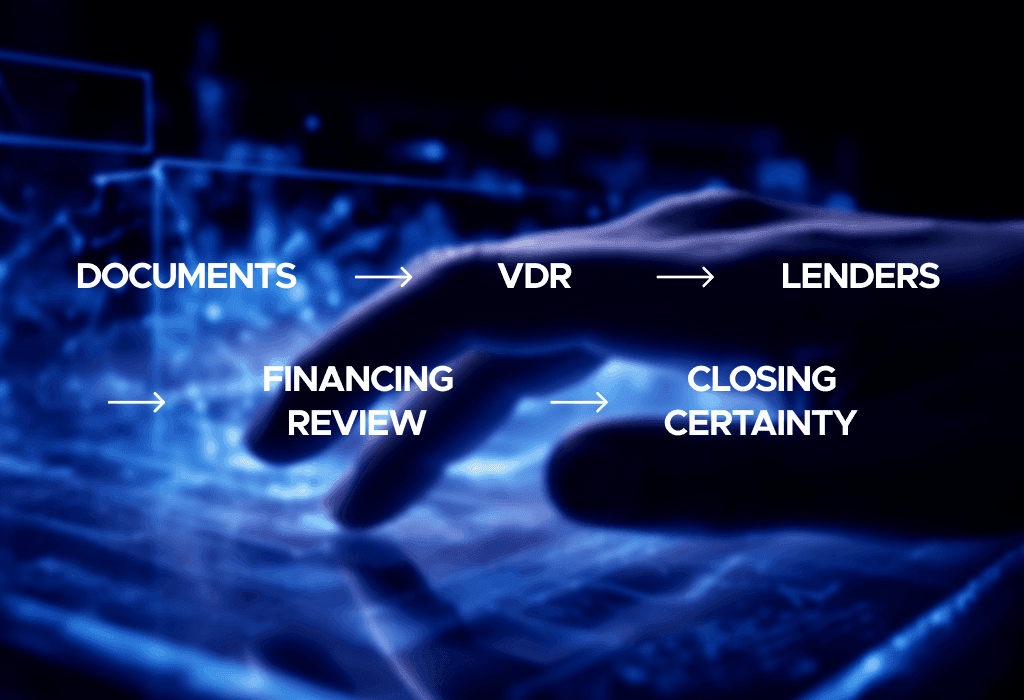

Financing due diligence tests whether the deal can be funded, closed, and serviced after completion. Lenders, investors, and buyers review financial statements, management accounts, tax returns, QoE reports, cash flow forecasts, working capital analysis, debt schedules, credit agreements, cap tables, and board approvals.

The buyer should prepare sources-and-uses schedules, acquisition debt models, term sheets, commitment letters, security documents, intercreditor drafts, equity commitment letters, SPA drafts, disclosure schedules, integration budgets, and synergy models. These materials support lender review of repayment capacity, collateral, and covenant headroom.

A virtual data room, or VDR, is essential because financing due diligence involves sensitive financial, legal, and commercial information. A structured VDR gives buyers, lenders, and advisers permissions, version control, Q&A workflows, and audit trails.

How Financing Terms Affect the Purchase Agreement

Financing terms directly affect the SPA. The agreement may include a financing condition, no-financing-condition language, source-of-funds representations, covenants to obtain financing, lender conditions, seller cooperation obligations, reverse termination fees, escrow or holdback mechanics, deferred consideration, and conditions precedent.

A financing condition allows the buyer to avoid closing if financing is unavailable. Sellers often resist broad conditions because they transfer funding risk to the seller. A buyer can improve closing certainty by providing committed debt, equity commitment letters, and limited lender outs. Where financing risk remains, the parties may negotiate a reverse termination fee.

Commitment letters should align with the SPA. Problems arise when the acquisition agreement requires closing, but financing documents include broader conditions, incomplete diligence requirements, or inconsistent timing. Security interests, repayment priority, pre-closing covenants, and post-closing restrictions should also be coordinated.

Risks and Red Flags in M&A Financing

Key risks include overleveraged structures, unrealistic synergies, weak free cash flow coverage, seasonal working capital pressure, tight covenants, uncertain lender commitment, maturity mismatch, and unresolved refinancing risk. Seller financing without clear default provisions, security, subordination, or set-off rules creates avoidable credit risk.

Earn-outs with vague metrics or buyer-controlled performance drivers can lead to post-closing disputes. Equity consideration with unclear valuation, poor liquidity, weak governance, or no exit route can be riskier than cash. These red flags show why financing should be tested before signing, not after closing.

FAQ

What are the main M&A financing methods?

The main methods are cash, debt, equity, and hybrid structures. Buyers often combine acquisition debt, sponsor equity, seller financing, rollover equity, and earn-outs to balance price, risk, and closing certainty.

How does debt financing work in an acquisition?

Debt financing provides capital through bank loans, private credit, bonds, or revolving credit facilities. The buyer must repay principal and interest, comply with covenants, and show service capacity.

What is equity financing in M&A?

Equity financing uses buyer shares, sponsor equity, minority investor capital, or stock-for-stock consideration. It reduces repayment pressure but dilutes existing owners and may expose sellers to valuation, liquidity, and governance risk.

What is hybrid financing in M&A?

Hybrid financing combines features of debt and equity. Mezzanine loans, preferred equity, seller notes, and earn-outs can fill funding gaps, but require clear rules on priority, payment, control rights, and accounting treatment.

How do seller notes and earn-outs work?

A seller note means the seller receives part of the price over time as a creditor of the buyer. An earn-out makes part of the price conditional on future performance, so metrics, reporting, and dispute procedures must be clear.

Which financing methods for mergers and acquisitions exclude borrowing?

Cash financing and equity financing can exclude borrowing if the buyer uses existing liquidity, issues shares, or raises investor capital without debt. These structures still involve trade-offs, including reduced cash reserves, dilution, and possible approval requirements.

What documents are needed for M&A financing due diligence?

Typical documents include financial statements, management accounts, QoE reports, forecasts, working capital analysis, debt schedules, cap tables, term sheets, commitment letters, security documents, board approvals, SPA drafts, and disclosure schedules. A VDR helps manage these materials securely with permissions, audit trails, and version control.

How does financing affect closing certainty?

Committed financing increases seller confidence by showing that funds should be available at completion. Uncertain debt, broad lender conditions, or weak source-of-funds evidence can reduce closing certainty and change SPA risk allocation.

Conclusion

M&A financing is a deal-structure decision, not only a funding exercise. The right mix balances cost of capital, control, dilution, leverage, covenants, seller protection, closing certainty, and flexibility. Strong financing due diligence and secure VDR workflows help translate the funding plan into clear SPA terms and reliable execution.