Key takeaways from the article

Emerging markets represent economies with high economic growth rates but persistent institutional immaturity and transitional regulatory systems.

Transactions in emerging markets differ from those in developed markets due to concentrated ownership, weaker corporate governance, and limited minority shareholder protections.

Political risk, regulatory risk, currency risk, and enforcement risk are the primary threats in cross-border deals, but can be substantially reduced.

Investors are drawn to emerging markets by superior growth potential, a persistent valuation gap, and strategic benefits such as market entry or resource access.

Effective participation requires adapted due diligence, reliance on local partners, and longer investment horizons than in mature economies.

Deal specifics demand a heavier focus on legal structuring, detailed representations & warranties, and strong post-closing controls.

The emerging markets category is highly diverse — no single template applies across countries or sectors.

What are emerging economies (emerging markets)?

Emerging markets are economies that exhibit rapid growth and increasing global integration, while institutions, legal systems, and financial markets remain underdeveloped compared to developed markets. Index providers — MSCI, FTSE Russell, S&P — classify them according to criteria including economic size, market liquidity, accessibility, and institutional strength. Typical constituents in 2025–2026 include China, India, Brazil, Indonesia, Mexico, South Africa, Turkey, Saudi Arabia, and several Southeast Asian and Eastern European countries.

What are emerging markets?

The definition of an emerging market identifies economies that combine above-average economic growth with ongoing institutional transition. They display features of both advanced and developing economies: expanding capital flows, rising foreign investment, and deepening trade links alongside institutional risk and incomplete market mechanisms.

Key distinguishing traits are:

GDP growth is persistently higher than in developed markets (frequently 4–7 % annually)

Institutional immaturity is evident in inconsistent contract enforcement and governance standards

Regulatory environment characterized by frequent amendments and variable application

Emerging markets differ markedly from developed markets, which possess stable institutions, high transparency, robust corporate governance, and deep, liquid capital markets. They also contrast with frontier markets — smaller, less liquid economies with greater infrastructural and political risks and very limited investability.

The term emerging markets designates an investment category rather than a uniform group of countries. Significant variation exists in political systems, resource dependence, state influence, financial market depth, and exposure to market volatility, making uniform strategies ineffective.

Common characteristics of emerging markets

Macroeconomic features typically include strong growth potential accompanied by pronounced market volatility, periodic inflation pressures, and exposure to global commodity and capital flows cycles.

The regulatory environment is often changeable — legislation and enforcement practices evolve rapidly, with noticeable enforcement gaps and selective implementation that increase uncertainty.

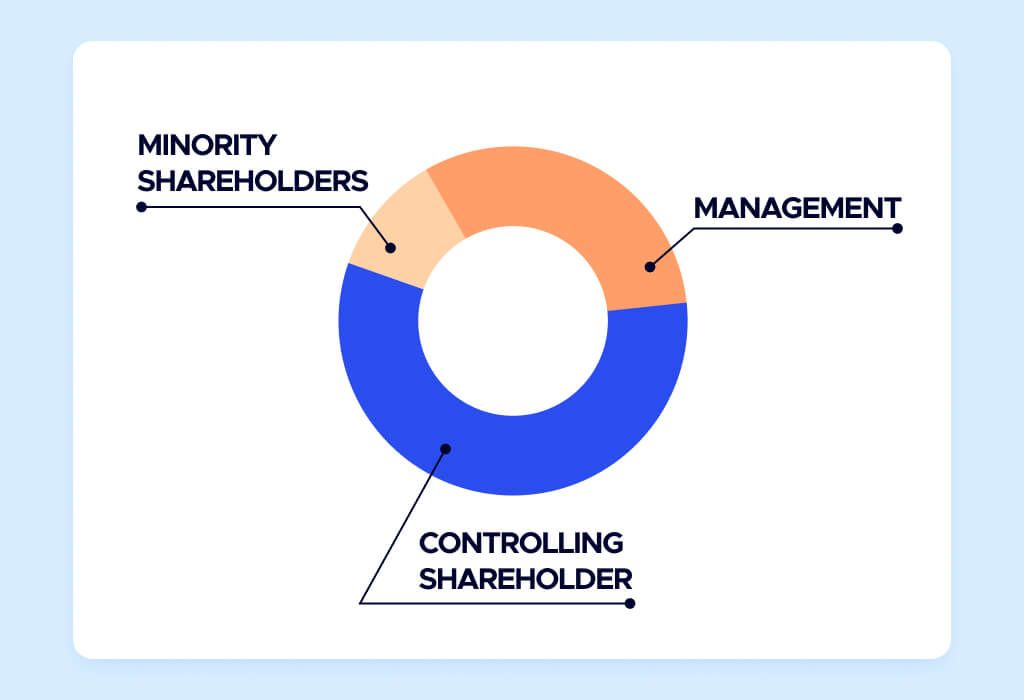

Corporate structures are predominantly family-owned companies or entities with substantial state influence, resulting in concentrated decision-making and limited separation between ownership and management.

Financial infrastructure ranges from moderately developed in larger economies to shallow in others, featuring restricted long-term capital access, bank-dominated financing, and underdeveloped bond or equity markets in many cases.

Information asymmetry and limited transparency remain widespread: financial disclosures can be incomplete, local accounting standards may diverge from international norms, and reliable operational data is frequently difficult to obtain or verify.

Deal specifics in emerging markets

Emerging market M&A and cross-border deals deviate from developed-market transactions primarily in ownership structure, corporate governance quality, and degree of minority shareholder protection. Ownership concentration — often in families, founders, or state hands — diminishes the relevance of models based on dispersed shareholders. Governance mechanisms frequently lack genuine independence, while safeguards for minority investors are comparatively weak.

Local partners and experienced local advisors play an indispensable role, providing insight into informal networks, regulatory interpretation, bureaucratic navigation, and relationship management essential for successful execution.

Deal documentation assigns exceptional importance to:

Meticulous legal structuring to address enforcement weaknesses.

Comprehensive representations & warranties compensating for disclosure deficiencies.

Reinforced post-closing controls, including board representation, veto rights, reporting obligations, and audit mechanisms.

The direct application of developed-market deal frameworks is usually ineffective. Differences in legal framework enforceability, judicial reliability, political interference potential, and information quality necessitate fundamentally customized transaction structuring rather than superficial adaptation.

Risks and risk mitigation in emerging market deals

Principal risk categories comprise political risk (abrupt policy reversals, expropriation signals), regulatory risk (mid-transaction rule changes, approval blocks), currency risk (exchange-rate depreciation, capital controls), and enforcement risk (limited or delayed access to legal remedies).

In practice, these risks appear as unexpected changes to sector regulations, sharp currency movements reducing returns, or prolonged inability to enforce contractual provisions through local courts or arbitration.

Risk-reduction instruments include sophisticated deal structuring techniques — staged payments, earn-outs, escrow arrangements, put/call options — as well as governance mechanisms such as supermajority approvals, independent directors, and detailed monitoring covenants.

Elevated risk levels do not inherently preclude transactions. When underlying growth prospects, entry valuations, and strategic rationale are attractive, and risks can be identified, quantified, and appropriately allocated, participation frequently yields superior long-term outcomes.

Why emerging markets attract investors despite complexity

Emerging markets continue to attract substantial foreign investment due to significantly higher long-term growth prospects than those of mature economies, which are constrained by demographics and saturation. A structural valuation gap persists, with assets trading at notable discounts that reflect institutional and volatility concerns but also embed an opportunity premium.

Strategic considerations further drive interest: early market entry into high-potential consumer bases, secure access to resources, supply-chain diversification, and long-term positioning in regions gaining global economic weight.

Participants who succeed maintain realistic expectations, accept extended holding periods — commonly 7–12 years — and calibrate return profiles to the transitional nature of these growth markets.

FAQ

What countries are considered emerging markets?

MSCI, FTSE Russell, and S&P classify countries such as China, India, Brazil, Indonesia, Mexico, South Africa, Turkey, Saudi Arabia, Malaysia, Thailand, Philippines, Chile, and Poland among emerging markets in 2025–2026. Classifications vary marginally between providers, with certain markets (e.g., South Korea, Taiwan) occasionally treated as developed.

Are emerging markets always high-risk?

No. Emerging markets generally exhibit higher political, currency, and institutional risks than developed markets, but the degree varies considerably by country and sector. Many have strengthened reserves, improved policy frameworks, and enhanced governance, resulting in risk profiles that are manageable for appropriately structured long-term investments.

How does due diligence differ in emerging markets?

Due diligence in emerging markets requires substantially greater emphasis on field-based verification, local intelligence, and qualitative analysis. It prioritizes assessment of controlling shareholder incentives, informal governance practices, regulatory change scenarios, and data reliability over purely financial and legal checks typical in developed markets.

Why are valuations often lower in emerging markets?

Valuations in emerging markets are typically lower due to elevated market volatility, governance concerns, enforcement uncertainty, and liquidity limitations. This valuation gap frequently offers an opportunity premium when investors can effectively manage or mitigate the associated risks.

Can foreign investors control businesses in emerging markets?

Foreign investors can obtain controlling stakes or full ownership in most sectors of emerging markets. Restrictions apply in strategic industries (energy, telecommunications, banking, defense) where ownership caps, mandatory local partners, or government pre-approval are common.

Conclusion

Emerging markets require a distinct approach to address specificities and transaction structuring that account for unique institutional risks, regulatory environments, and corporate governance characteristics. Attempts to apply simplified or imported frameworks from developed markets rarely succeed. Investors who adapt strategies, leverage local partners, implement robust risk mitigation, and commit appropriate time horizons can capture the substantial growth and positioning advantages these growth markets continue to offer in the global economy.