Key Takeaways from the Article

M&A valuation establishes a realistic range of values rather than one precise figure: models provide boundaries, while the final price is driven by negotiation power and each side's leverage.

DCF calculates intrinsic value by discounting projected cash flows, but outcomes depend heavily on assumptions about growth rates and WACC, so practitioners often favor faster market-based methods in time-sensitive deals.

Comparable companies and precedent transactions reflect actual market pricing, including control premiums of 25–40%, requiring adjustments for differences in scale, profitability, and industry conditions.

Strategic buyers consistently pay more than financial buyers because they can capture synergies such as 15–40% cost savings or revenue growth that standalone models do not account for.

Due diligence commonly reduces the initial valuation through adjustments to earnings quality, working capital levels, and undisclosed liabilities, keeping the process fluid until closing.

The final transaction price deviates from model results due to deal structure (earn-outs, deferred payments), market timing, auction pressure, and non-financial buyer motives such as blocking rivals or gaining technology access..

How to value mergers and acquisitions determines what an acquirer is willing to pay for control of the target. Unlike routine financial appraisals, M&A valuation is forward-looking, negotiation-driven, and heavily influenced by synergies and risk allocation. The intrinsic estimate from discounted cash flows often diverges from market-implied values and the negotiated price, which typically embeds a premium for gaining full ownership and influence.

What Company Valuation Means in the M&A Context

Valuation in mergers and acquisitions establishes the enterprise or equity value of the target specifically for the transaction. The emphasis lies on the price that will secure control, incorporating expected benefits from combining operations. Intrinsic value estimates the company's worth based on its standalone cash-generating ability, most often through DCF analysis. Market value captures what similar publicly traded firms command today via trading multiples. The actual deal price—the amount agreed upon—usually exceeds the pre-announcement trading level by 25–40% to reflect the control premium and strategic advantages.

Valuation serves primarily as a negotiation dynamic rather than a fixed truth. Analytical models produce a credible range, but the outcome hinges on relative power (exclusive processes, alternative bidders, funding security), timing pressures, and how well the deal fits the acquirer's strategy. Buyers advocate conservative forecasts and highlight risks; sellers stress growth opportunities and cost efficiencies. Advisors from investment banking help both sides build cases by blending approaches to support their stance at the table.

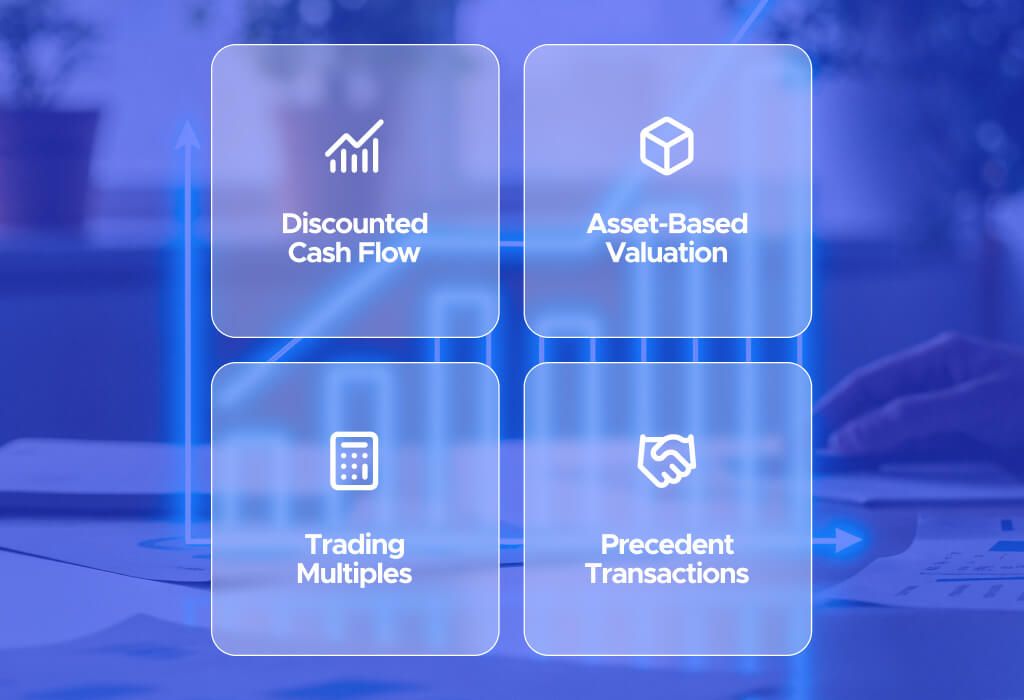

Core Valuation Methods Used in M&A

Discounted Cash Flow (DCF)

DCF derives value by estimating future free cash flows, discounting them to present terms with the weighted average cost of capital (WACC), and appending a terminal value. The core equation sums discounted periodic flows plus a capitalized residual: Present Value = Σ (FCF_t / (1 + WACC)^t) + Terminal Value / (1 + WACC)^n. Terminal value typically uses perpetual growth (FCF next year / (WACC–g)) or an exit multiple.

Critical inputs encompass credible projections for revenue expansion, operating margins, reinvestment needs, WACC (factoring equity and debt costs plus risk adjustments), and long-term growth (commonly 2–3% for established firms). Advantages include a focus on fundamental cash generation and suitability for predictable businesses. Drawbacks involve heavy reliance on subjective forecasts—a modest shift in discount rate or growth can alter results substantially—and reduced applicability for high-volatility or nascent companies.

How to value a company for acquisition through DCF focuses on long-term cash flows and suitability for businesses with predictable performance.

Comparable Companies Analysis (Trading Multiples)

This technique applies multiples from similar listed companies to the target's metrics. Frequently used ratios include EV/EBITDA, P/E, EV/Revenue, and price-to-sales. Steps involve identifying peers matching industry, scale, region, and growth characteristics; deriving median or mean multiples; applying them to derive enterprise value; then deducting net debt for equity value.

Constraints arise from market mood swings that distort ratios, challenges in securing exact matches, omission of firm-specific factors like synergies or risk assessments, and pronounced fluctuations in cyclical sectors.

Precedent Transactions

Precedent analysis examines multiples from recent comparable acquisitions (EV/EBITDA, EV/Revenue, etc.), capturing premiums paid for control and transaction nuances. It differs from trading multiples by including those premiums (typically 25–40%) and deal circumstances. Adjustments account for shifts in market sentiment, relative scale, and strategic elements since the prior deals.

Asset-Based Valuation

This method tallies fair values of assets (tangible plus intangible) minus obligations, either as a going concern or liquidation scenario. It proves most useful for asset-intensive sectors like real estate or resources, or in turnaround situations. For ongoing operations, it tends to understate value from intangibles such as brands, customer loyalty, and proprietary know-how.

Key Value Drivers in M&A Deals

Financial elements include revenue trajectory, EBITDA margins, cash flow reliability, and debt levels relative to earnings. Strong profitability, efficient capital use, and robust cash conversion support elevated pricing.

Operational aspects cover scalability (particularly in tech or subscription models), customer dependency risks (one client exceeding 20% revenue flags concern), retention metrics, and supply chain vulnerabilities.

Strategic considerations often drive the largest differentials: cost synergies (frequently 15–40% of target expenses), revenue enhancements, market entry, intellectual property, and technological edges. Strategic purchasers can justify 20–50% higher bids by capturing these gains, whereas financial purchasers emphasize standalone performance and resale potential.

Risk factors that depress offers encompass regulatory obstacles (antitrust scrutiny), legal exposures, reliance on key personnel, and data security weaknesses. Identical assets yield varied bids—a strategic acquirer sees combined upside, a financial sponsor targets cash flows plus exit value, and a distressed buyer may limit assessment to asset recovery.

Why Deal Price Differs from Valuation Models

Models outline a plausible band, but the closing figure emerges from bargaining strength. The advantaged side—buyer in a soft market or seller with multiple suitors—secures better terms.

Control premium accounts for much divergence: acquirers pay 25–40% above recent trading levels to secure decision-making authority.

Transaction mechanics influence outcomes: pure cash delivers certainty and often lower multiples; equity introduces share-price risk; earn-outs and deferred elements reconcile differing forecasts.

Market conditions matter: buoyant environments inflate premiums through competition; downturns encourage discounts.

Non-quantitative drivers—preventing rivals from gaining ground, locking in resources, or competitive pressure in auctions—regularly propel prices beyond calculated ranges.

Valuation Adjustments During Due Diligence

Due diligence regularly revises preliminary valuations. Standard modifications address earnings quality (stripping non-recurring items to normalize EBITDA), working capital variances (aligning to agreed pegs with cash adjustments), and off-balance-sheet obligations (leases, incentives, contingencies).

Valuation evolves continuously from initial indications through signing to closing. Material discoveries can cut the price 10–30% or prompt structures like earn-outs, holdbacks, or termination rights. Advisors safeguard interests by scrutinizing data rooms, quantifying impacts, and negotiating protective provisions.

FAQ

Is DCF always the most accurate valuation method?

No. DCF offers a robust intrinsic perspective but depends critically on forecast accuracy and discount assumptions. For volatile, growth-oriented, or cyclical businesses, market-derived methods (comparables and precedents) frequently prove more dependable as they mirror investor willingness to pay. Blending approaches yields the strongest outcomes.

How do synergies affect acquisition price?

Synergies—cost reductions (often 15–30% of target expenses) and revenue opportunities—enable strategic buyers to support premiums of 20–50% over standalone estimates. Buyers embed these advantages in their post-transaction models, expanding the affordable range. Financial buyers, lacking synergy realization, align closer to market multiples.

Who determines the final valuation in M&A deals?

Buyer and seller negotiate the price, informed by bankers, counsel, and specialists. Models establish a reference range, but bids, leverage, diligence results, and strategic goals ultimately set the closing amount.

Can valuation change after signing the term sheet?

Yes, sometimes substantially. Diligence between signing and closing uncovers discrepancies leading to price cuts, contingent payments, escrow increases, or deal termination. Material adverse change provisions shield buyers from major declines.

Why do similar companies sell at different multiples?

Comparable firms command varying multiples due to contrasts in growth expectations, earnings stability, customer risks, synergy potential, prevailing market tone, and bargaining positions. Precedents reflect control premiums; trading multiples show public sentiment; unique exposures reduce value.

Conclusion

M&A valuation methods as a practical aid for informed choices rather than an exact science. Analytical tools supply structure, yet the transaction price arises from synergies, uncertainties, bargaining realities, and payment terms. Grasping these layers enables buyers to avoid excess costs and sellers to capture fair value, fostering deals that deliver lasting benefits for both parties.