Key Takeaways

Working capital in M&A is a negotiated pricing metric, not just a standard balance sheet calculation.

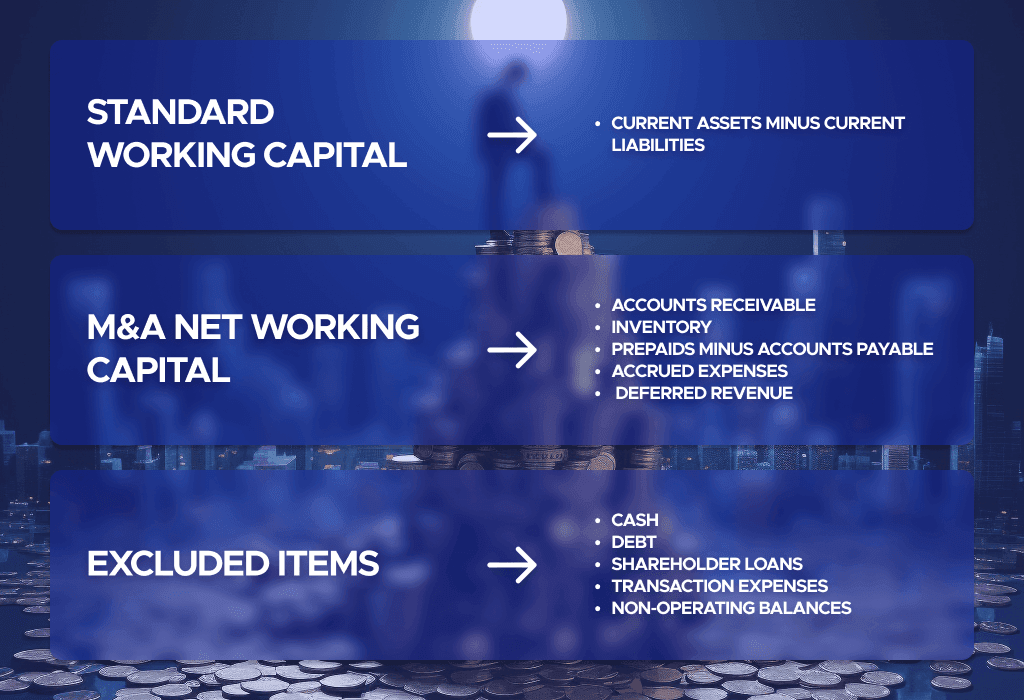

Net Working Capital (NWC) usually includes current operating assets and liabilities, while excluding cash, debt, and non-operating items.

A Working Capital Peg sets the target level of operating capital the buyer expects to receive at closing.

The purchase price adjustment can increase or reduce seller proceeds depending on the closing working capital versus the agreed target.

Most disputes arise from accounting policies, inventory, deferred revenue, accruals, and unclear included or excluded accounts.

Due diligence, SPA definitions, and data room documentation reduce the risk of post-closing disputes.

In M&A transactions, working capital affects more than financial reporting; it directly changes the final purchase price. Buyers expect enough operating liquidity on Day One, while sellers want compensation for excess capital left in the company. Disputes often arise from included or excluded items, seasonal movements, accounting policies, and closing accounts.

What Is Working Capital in M&A?

Working capital (WC) represents the baseline liquidity a business needs for everyday operations ($\text{Current Assets} - \text{Current Liabilities}$). In M&A, however, the definition is narrower and heavily negotiated: parties focus strictly on Net Working Capital (NWC), which isolates operating assets and liabilities to reflect pure operational reality. This is critical because modern acquisitions are typically structured on a cash-free, debt-free basis, meaning financing decisions, shareholder balances, and cash piles are stripped out to evaluate the business purely on its organic trading health.

The buyer expects to receive a business with sufficient operating capital on Day One to trade normally without an immediate cash injection, while the seller demands fair compensation for any excess liquidity left behind. To balance these interests, NWC is built into the purchase price adjustment mechanism, making the SPA accounting schedules (defining included/excluded accounts and a normalized Target WC) just as vital to CFOs, buyers, and legal advisers as the headline valuation.

NWC is never analyzed in a vacuum; transaction advisers review it alongside EBITDA, Quality of Earnings (QoE), debt, and cash to prevent accounting manipulation.

How Working Capital Is Calculated in M&A

The usual starting point is:

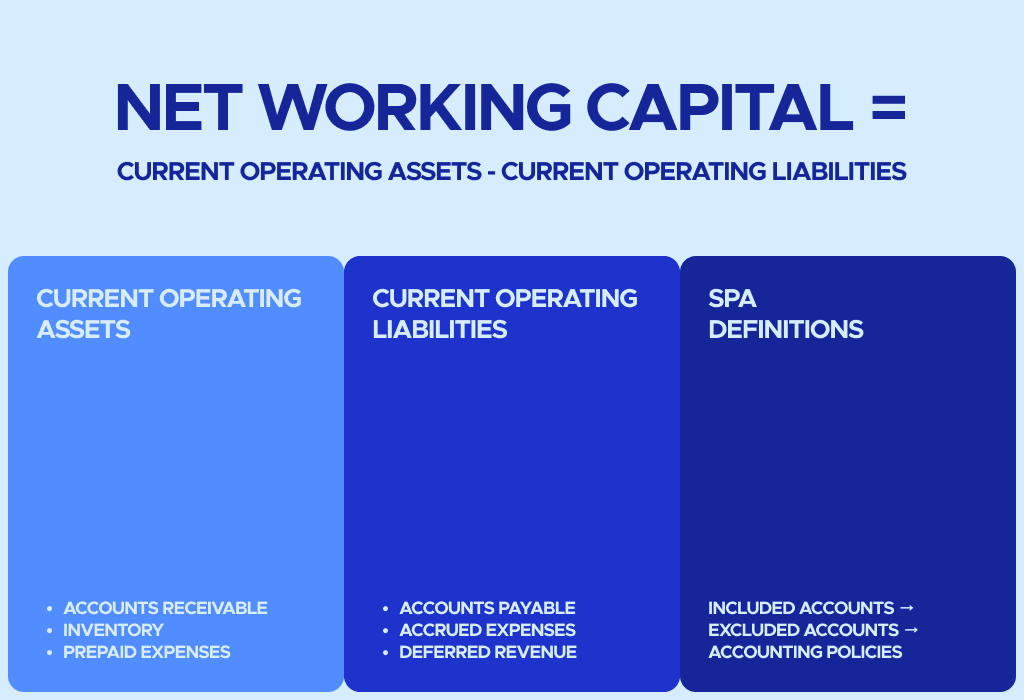

Net Working Capital = Current Operating Assets - Current Operating Liabilities

The formula is simple, but the M&A calculation is not automatic. Not every current asset or current liability is included. The SPA should state exactly which accounts count toward NWC and how they are measured.

Current Operating Assets: Often include accounts receivable, inventory, and certain prepaid expenses. Accounts receivable are amounts owed by customers for delivered goods or services. Buyers review aging reports for overdue balances, bad debt risk, and unusual collection patterns. Inventory may include raw materials, work in progress, and finished goods, but buyers test for obsolete, slow-moving, or overstated stock. Prepaids may be included if they create a future operating benefit.

Current Operating Liabilities: Usually include accounts payable, accrued expenses, and, in some deals, deferred revenue. Accounts payable show amounts owed to suppliers. Buyers review AP aging to see whether payments were delayed before closing. Accrued expenses cover costs incurred but not yet paid, such as payroll, utilities, bonuses, and certain taxes. Deferred revenue is negotiated because the business has received cash but still owes future delivery.

Common exclusions include cash, bank debt, credit facilities, accrued interest, current portions of long-term debt, shareholder loans, transaction expenses, non-operating assets, and one-off liabilities. These are normally addressed in the cash-free, debt-free structure or net debt adjustment.

Global Precedent: A recent example is the Save Mart / Kingswood Capital dispute, reported by the Financial Times. After Kingswood acquired the California supermarket chain Save Mart, the buyer sought a $109 million post-closing adjustment linked to how debt and balance-sheet items were treated under the purchase agreement.

What Is a Working Capital Peg?

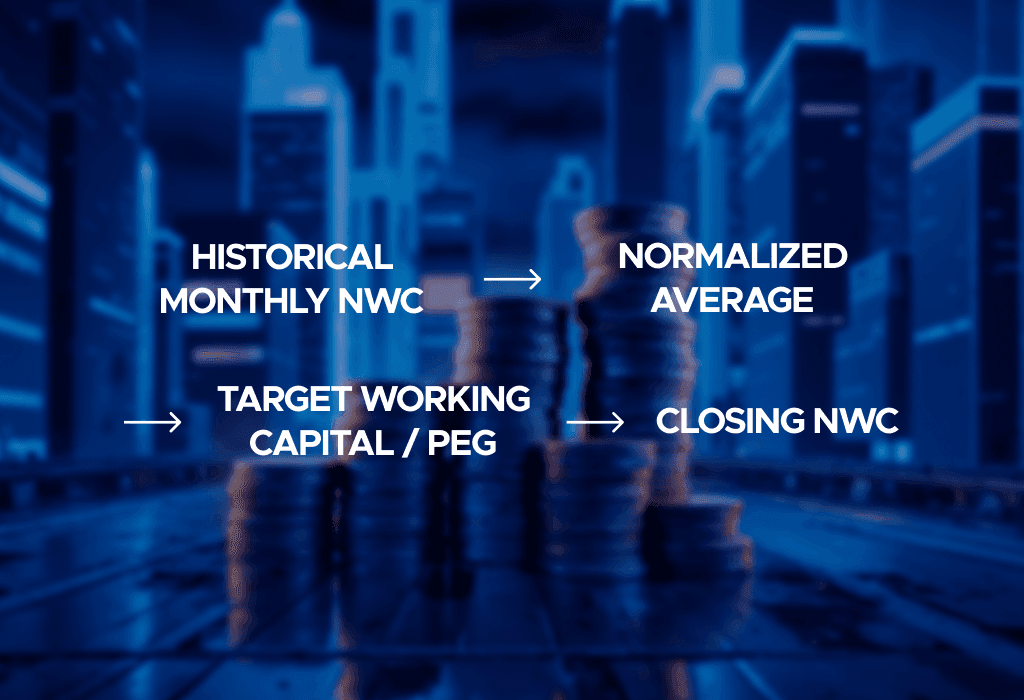

The Working Capital Peg (or Target Working Capital) is the agreed benchmark used to test whether a business is delivered with a normal level of operating liquidity at closing. Closing NWC is compared against this target to determine whether the final purchase price moves up or down.

Because a single balance sheet date can reflect temporary anomalies, due diligence teams analyze 12 to 24 months of data to calculate a historical average or normalized working capital benchmark. Transaction advisers must calibrate this Peg against seven critical factors:

Seasonality (pre-peak inventory build-up) and revenue growth/decline (scaling asset requirements).

Shifting customer payment terms or supplier payment cycles (stretching or compressing cash).

Strategic inventory build-up and recent changes in accounting policies.

Tactical one-off actions before closing (like accelerated collections or delayed vendor payments).

The Peg is heavily negotiated because it directly shifts economic value between parties. If it is set too high, the seller is penalized with an unfair downward price adjustment; if it is too low, the buyer receives an undercapitalized business and is forced to make an immediate cash injection on Day Two, effectively overpaying for the acquisition.

How Working Capital Affects Deal Price

Working capital directly affects the final deal price through the post-closing adjustment mechanism. Once the parties agree on the Target Working Capital, the actual closing NWC is measured and compared against this benchmark:

If closing working capital is higher than the target: The seller is usually entitled to an upward adjustment, increasing the final purchase price. This protects sellers from transferring excessive operating capital without compensation.

If closing working capital is lower than the target: The purchase price is typically reduced dollar-for-dollar. This protects buyers from inheriting an undercapitalized business and prevents the seller from artificially draining liquidity (e.g., stripping inventory or delaying vendor payments) right before handover.

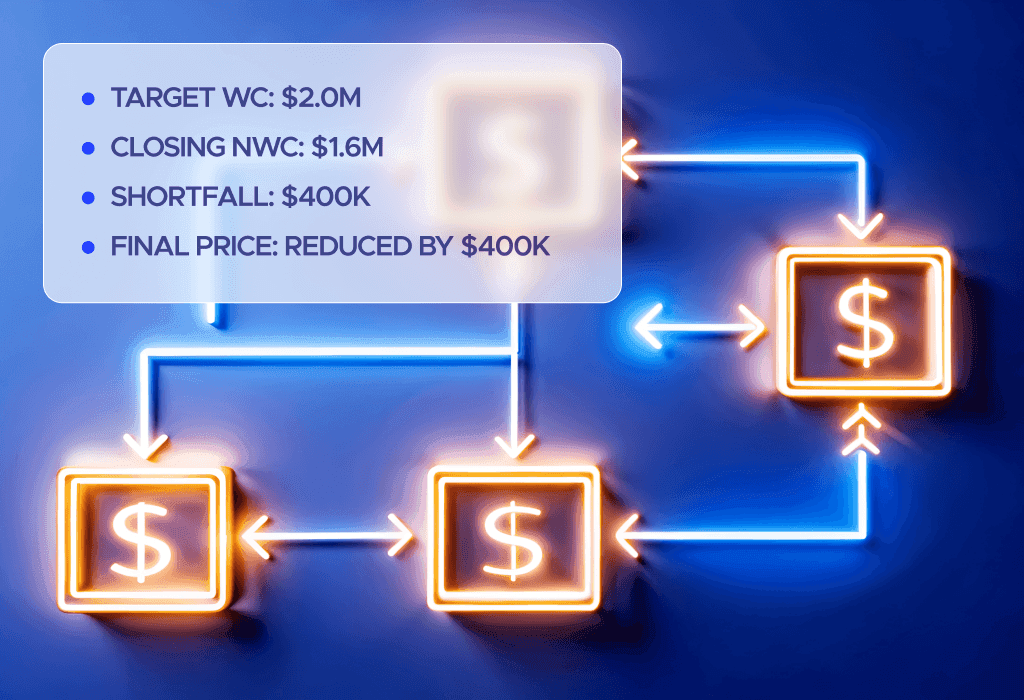

Example of a Dollar-for-Dollar Adjustment:

Target Working Capital: $2.0 million

Actual Closing NWC: $1.6 million

Adjustment: $400,000 shortfall

In this scenario, the purchase price is automatically reduced by $400,000. The buyer pays less at closing because they will immediately need to inject that exact amount of cash into the business on Day Two to restore normal operations. Conversely, if closing NWC came in at $2.2 million, the seller would receive an extra $200,000 at settlement.

Working Capital Adjustment Mechanisms

The exact mechanism depends on the SPA and the deal structure.

Closing Accounts Mechanism: The buyer prepares closing accounts upon completion to calculate the actual cash, debt, and NWC as of the closing date. The price is then true up against the agreed targets. This approach can be accurate, but it often creates disputes over definitions, classifications, and accounting methods.

Locked Box Mechanism: The purchase price is fixed by reference to financial statements at an agreed locked box date. The seller normally keeps the economic benefit of trading between that date and closing, but must not extract unauthorized value from the business. Because there is usually no broad true-up, buyers rely more on due diligence and leakage protections.

In cash-free, debt-free deals, working capital is only one part of the pricing bridge. Enterprise value, cash, debt, and NWC are separate but connected calculations. Working capital measures operating liquidity, while cash and debt adjustments deal with financing-related items.

Where a post-closing adjustment applies, the SPA should set deadlines, review rights, documentation requirements, and dispute procedures. Escrow or holdback arrangements may keep funds available until the adjustment is final. If the parties cannot agree, the SPA often refers disputed items to an independent accountant or expert.

The definition schedule is often more important than the headline formula. It should specify the treatment of deferred revenue, bonuses, taxes, transaction expenses, customer deposits, related-party balances, and inventory reserves. A structured Virtual Data Room (VDR) should store working capital schedules, trial balances, AR and AP aging, inventory reports, and support files.

Common Disputes and Red Flags in Working Capital Analysis

Working capital disputes typically erupt when the closing calculation deviates from normal, historical operating practice. To prevent post-closing litigation, deal teams must identify these critical red flags during financial due diligence, rather than after the final adjustment notice is delivered.

The Most Common Operational Red Flags:

Manipulated Cash Cycles: Aggressive collection of receivables right before closing (offering unusual discounts or rushing customers) artificially deflates the AR balance. Conversely, delayed payments to suppliers expand AP, masking the company's true, ongoing cash requirements.

Inflated Asset Values: Inventory overstatement via obsolete, slow-moving, or damaged stock artificially swells NWC, forcing the buyer to pay for dead assets.

Aggressive Accounting Shifts: Sudden changes in revenue recognition or the treatment of deferred revenue (which can be classified as an operational liability or a debt-like item depending on future fulfillment costs) can easily distort the target peg.

Hidden Liabilities: Unclear treatment of related-party balances, unrecorded employee bonuses, payroll accruals, transaction expenses, litigation reserves, and complex tax obligations often slip through standard accounting filters.

Impact on the Transaction Strategy:

Valuation & SPA Negotiations: Distortions in NWC often signal deeper issues in EBITDA accuracy, directly impacting the initial headline enterprise valuation and triggering aggressive pushes for a lower price or a higher Target Peg.

Escrow & Indemnities: High-risk accounts (like pending tax audits or uncollectible AR) force buyers to negotiate larger escrow holdbacks and specific, robust indemnities to shield themselves from post-closing leakage.

Post-Closing Disputes: Inconsistent accounting policies used right before handover serve as the number-one trigger for expensive, protracted post-closing arbitration, transforming what should be a routine true-up into a multi-million dollar legal battle.

How Buyers and Sellers Prepare Working Capital Documentation

Preparation is the key to avoiding post-closing disputes. Successful transactions rely on a rigorous, data-driven approach by both sides long before the SPA is signed.

The Buyer’s Due Diligence Approach

Buyers must move beyond surface-level figures to validate the underlying quality of the working capital:

Deep-Dive Analytics: Perform a thorough review of historical monthly working capital and analyze AR/AP aging reports alongside inventory turnover.

Consistency Testing: Rigorously test the consistency of accounting policies to ensure figures aren't being "massaged" through reserve changes.

Trend & Seasonality Correlation: Compare working capital movements against revenue trends and seasonal peaks to ensure the operating cycle makes logical sense.

Peg Validation: Stress-test the proposed Target WC peg and the specific SPA adjustment language to ensure they accurately reflect the business's true economic needs.

The Seller’s Preparation Strategy

Sellers can significantly accelerate the deal timeline and protect their valuation by being proactive:

Clean Data Sets: Prepare clear, monthly schedules that reconcile the trial balance to the management accounts.

Proactive Transparency: Identify and explain unusual movements beforehand; clearly separate operating from non-operating items to avoid unnecessary "debt-like" reclassifications by the buyer.

VDR Excellence: Store all supporting files (invoices, reports, policy documents) in a structured Virtual Data Room.

High-quality preparation translates directly into smoother negotiations. When financial analysis is backed by transparent, structured documentation, it becomes effortless to translate those insights into precise SPA terms, clear adjustment examples, and robust accounting schedules.

A well-known due diligence example is Hewlett-Packard’s acquisition of Autonomy. After buying the UK software company for $11.1 billion, HP later recorded an $8.8 billion write-down and alleged that Autonomy’s value had been inflated through serious accounting improprieties.

FAQ

What is working capital in M&A?

Working capital in M&A is the operating capital a buyer expects to receive with the business at closing. It is usually negotiated in the SPA and may directly affect the final purchase price.

How is net working capital calculated in an acquisition?

Net working capital is commonly calculated as current operating assets minus current operating liabilities. The exact calculation depends on negotiated definitions, excluded items, and accounting policies.

What is a working capital peg?

A working capital peg is the target level of NWC agreed by the buyer and seller. Closing working capital is compared with this target to calculate any purchase price adjustment.

How does working capital affect the purchase price?

If closing working capital is below the target, the purchase price may be reduced. If it is above the target, the seller may receive an increase, depending on the SPA.

What is excluded from working capital in M&A?

Cash, bank debt, shareholder loans, accrued interest, transaction expenses, and non-operating balances are commonly excluded. The exact exclusions must be stated in the purchase agreement.

Why do working capital disputes happen after closing?

Disputes happen when parties disagree on included accounts, accounting policies, reserves, deferred revenue, or closing accounts. Clear definitions and organized support documents reduce this risk.

Conclusion

Working capital is not a minor accounting detail in M&A. It is a direct pricing mechanism that can change buyer cost and seller proceeds. Accurate definitions, historical analysis, and consistent accounting policies help align price with economic reality. A structured due diligence process and well-managed data room make the adjustment process easier to evidence and less likely to end in dispute.